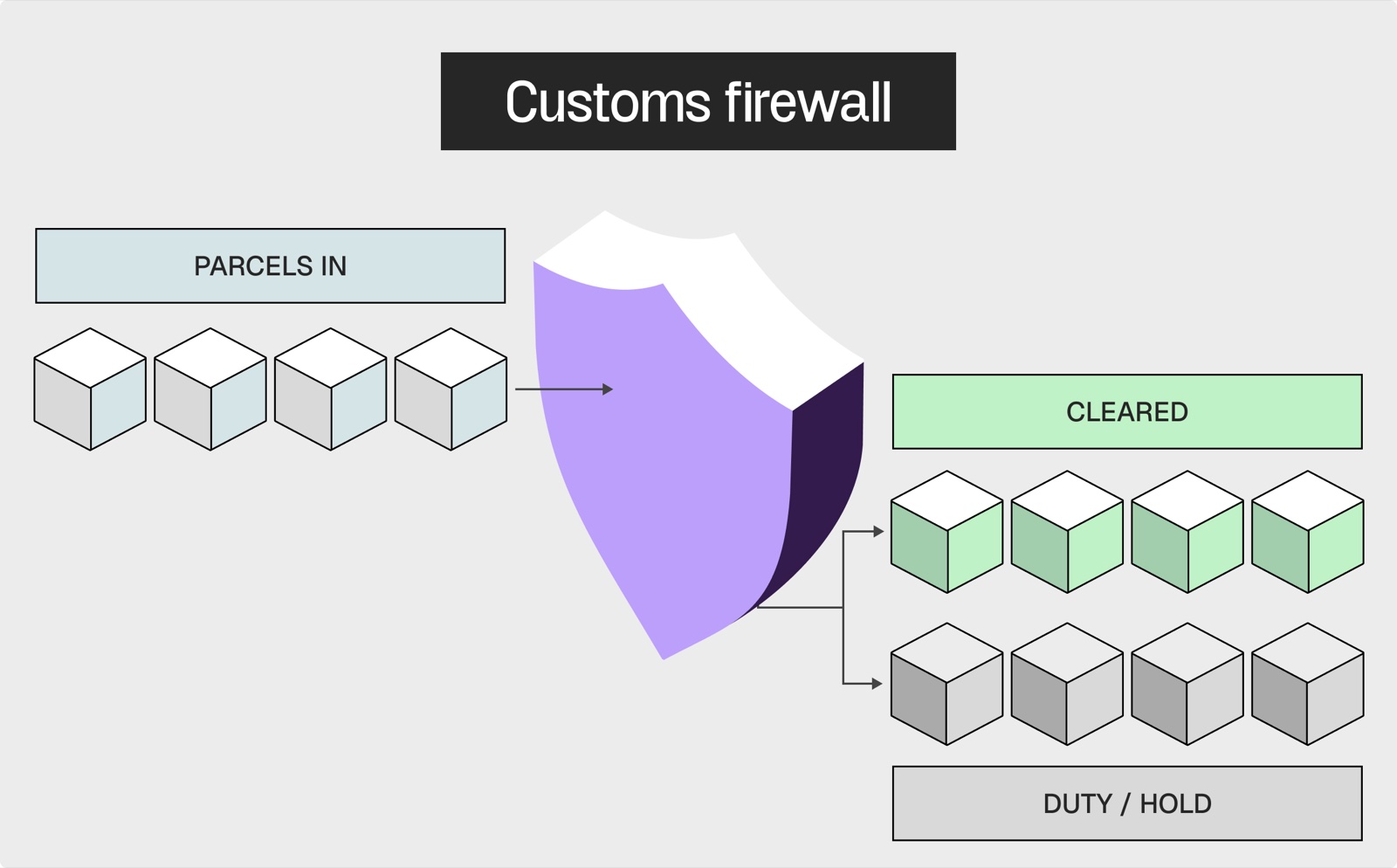

Customs is the physical world’s firewall. It inspects what crosses a border, checks it’s legal, and collects duty and import tax before letting it in. For two decades, anything under €150 entering the EU mostly waved straight through. On 1 July 2026, that stops — every parcel now faces a charge.

This is the biggest shift in cross-border physical-goods economics in a decade. Here’s customs from first principles, and what the reform actually changes.

In short: The EU is abolishing its €150 de minimis duty exemption on 1 July 2026. An interim €3 flat duty per item-category applies straight away, a ~€2 handling fee is expected around November, and from 2028 the platform — not the shopper — becomes the legal importer. Winners price the landed cost honestly at checkout instead of ambushing the buyer at the door.

What is customs, and why does it exist?

Customs is the government process that inspects goods crossing a border, validates they’re safe and legal, and collects import duty and import VAT. Every country runs one — the Douane (Netherlands), HMRC (UK), CBP (US), Zoll (Germany). Different names, identical logic.

It exists for three reasons: revenue (tariffs are state income), trade policy (duties protect domestic producers), and safety (keeping out the dangerous and counterfeit).

The key thing: customs is deterministic. It doesn’t negotiate — it reads structured data and fires rules. That’s why the EU reform matters: it’s an upgrade to the rule engine, and it pushes the legal liability onto whoever sells the goods.

Import duty vs import VAT: the words you need

Six terms and you can follow the rest:

| Term | What it means |

|---|---|

| Import duty | A tax on imported goods (% of customs value). A sunk cost — you never get it back. |

| Import VAT / GST | Consumption tax at the border, same rate as buying locally. Businesses can usually reclaim it. |

| HS code | A global 6-digit product code (EU extends to 10 and occasionally more). It decides the duty rate. |

| Customs value | The value duty is calculated on — usually CIF: goods + freight + insurance. |

| De minimis | The threshold below which duty is waived. The EU’s €150 threshold ends 1 July 2026. |

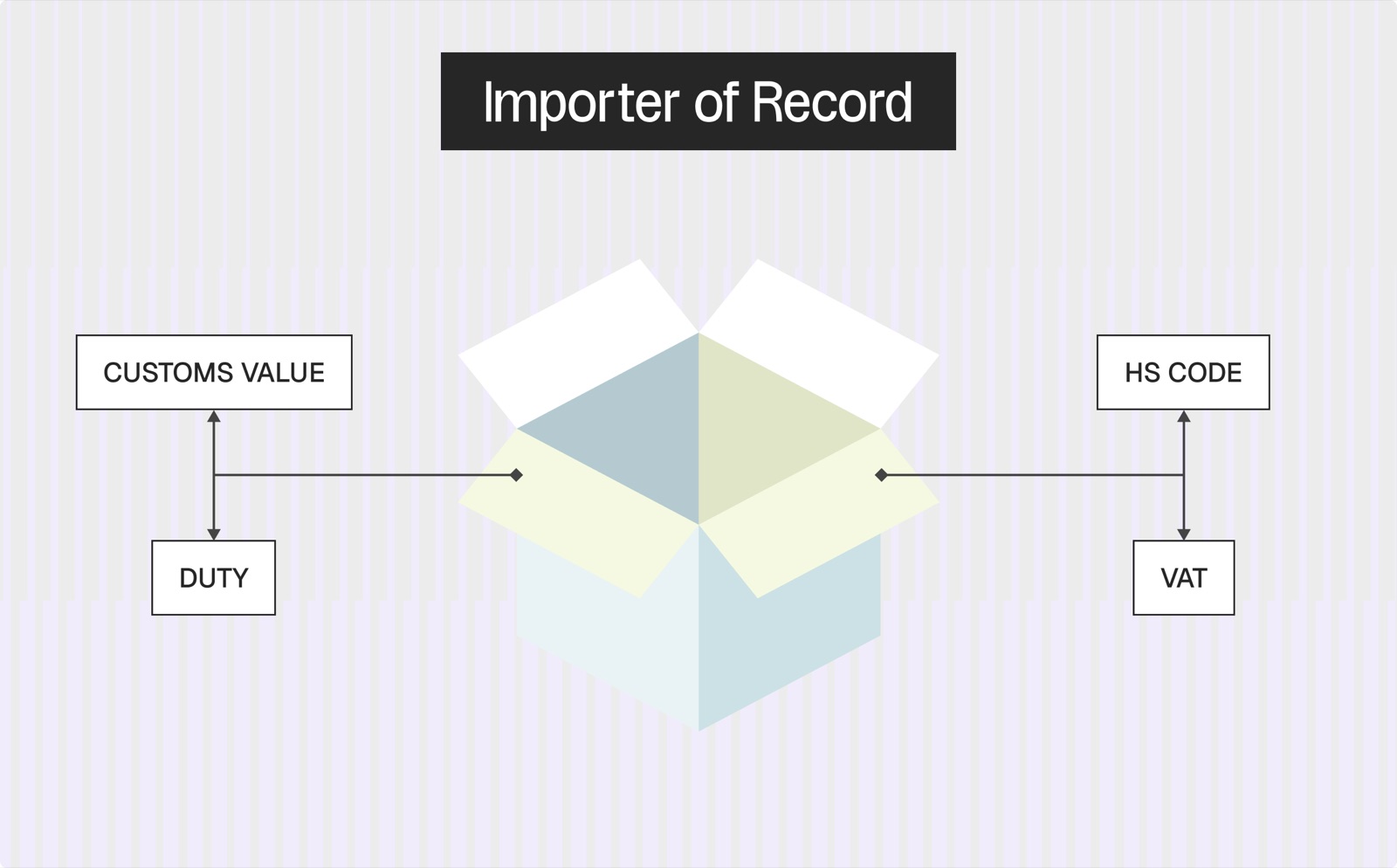

| Importer of Record (IOR) | The entity legally on the hook for compliance and paying duty — buyer, seller, or platform. This is the one that matters. |

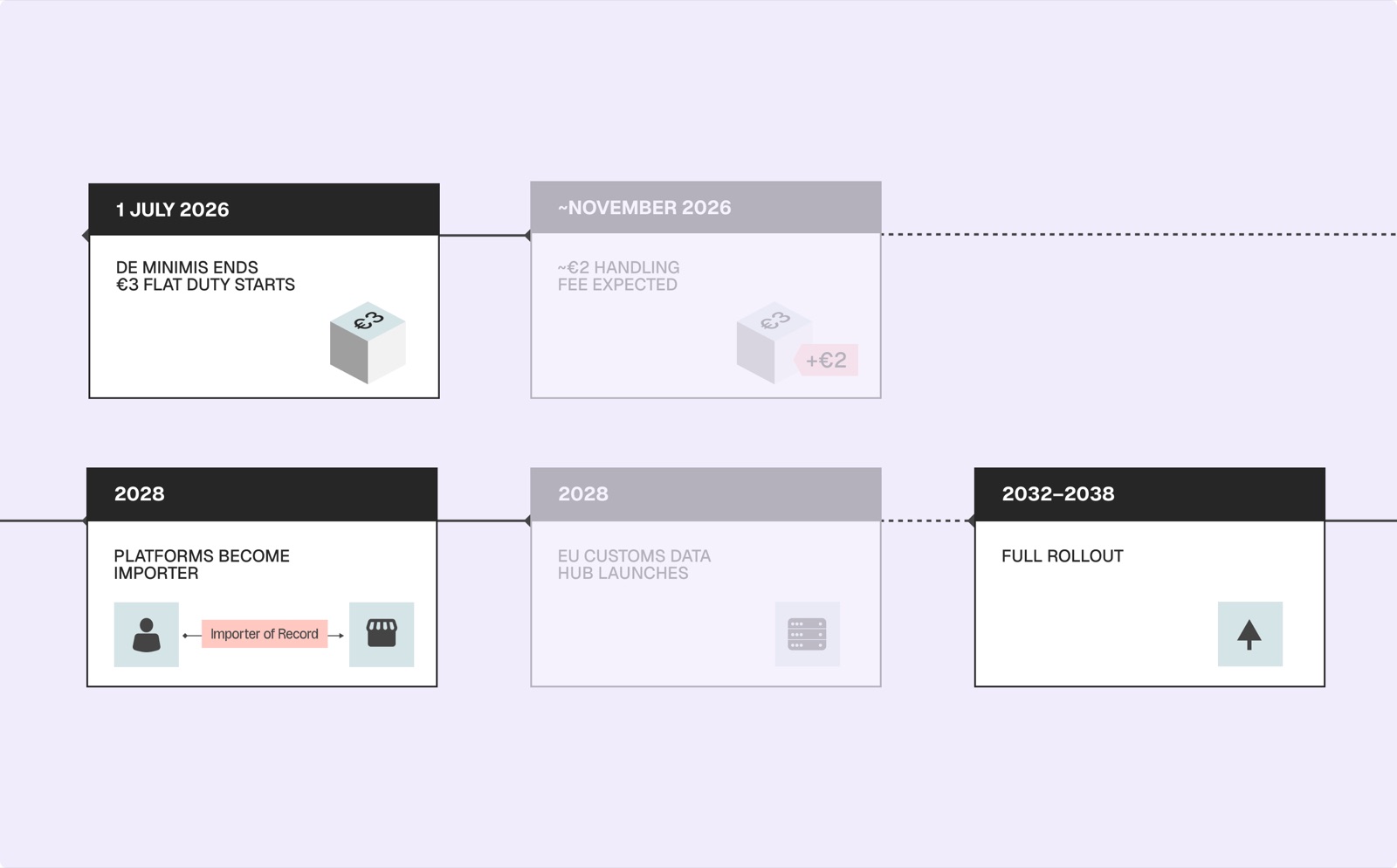

What changes on 1 July 2026?

Why now? Scale. Around 4.6 billion parcels under €150 entered the EU in 2024 — roughly 91% from China — about 12.6 million a day. Add systematic undervaluation to stay under €150, and the old manual model simply broke. So the EU is shipping a phased upgrade:

- 1 July 2026 — de minimis abolished. Every parcel faces duty. An interim €3 flat duty per item-category (per tariff line, not simply per parcel) bridges the gap. (Council approved 11 Feb 2026; regulation published 30 April; EC guidance issued 2 June. The per-item vs per-consignment basis is still being clarified — confirm before quoting a merchant a precise figure.)

- ~November 2026 — a ~€2 Union handling fee per parcel is expected on top, pushing a low-value parcel to a ~€5 baseline before VAT. (Signalled, not finally fixed; France already runs its own €2-per-item version, live since 1 March 2026.)

- 2028 — the deemed-importer rule. Platforms (Amazon, Temu, Shein) become the legal importer and collect duty and VAT at checkout. The surprise bill at the door ends by law.

- 2028 — the EU Customs Data Hub goes live for e-commerce, run by the new EU Customs Authority in Lille. Flat interim duty gives way to classification-based duty. (A simplified low-value tariff of roughly 5/8/12/17% has been proposed — it is a design concept, not adopted law.)

- 2032–2038 — full rollout to all importers; national legacy customs systems switched off.

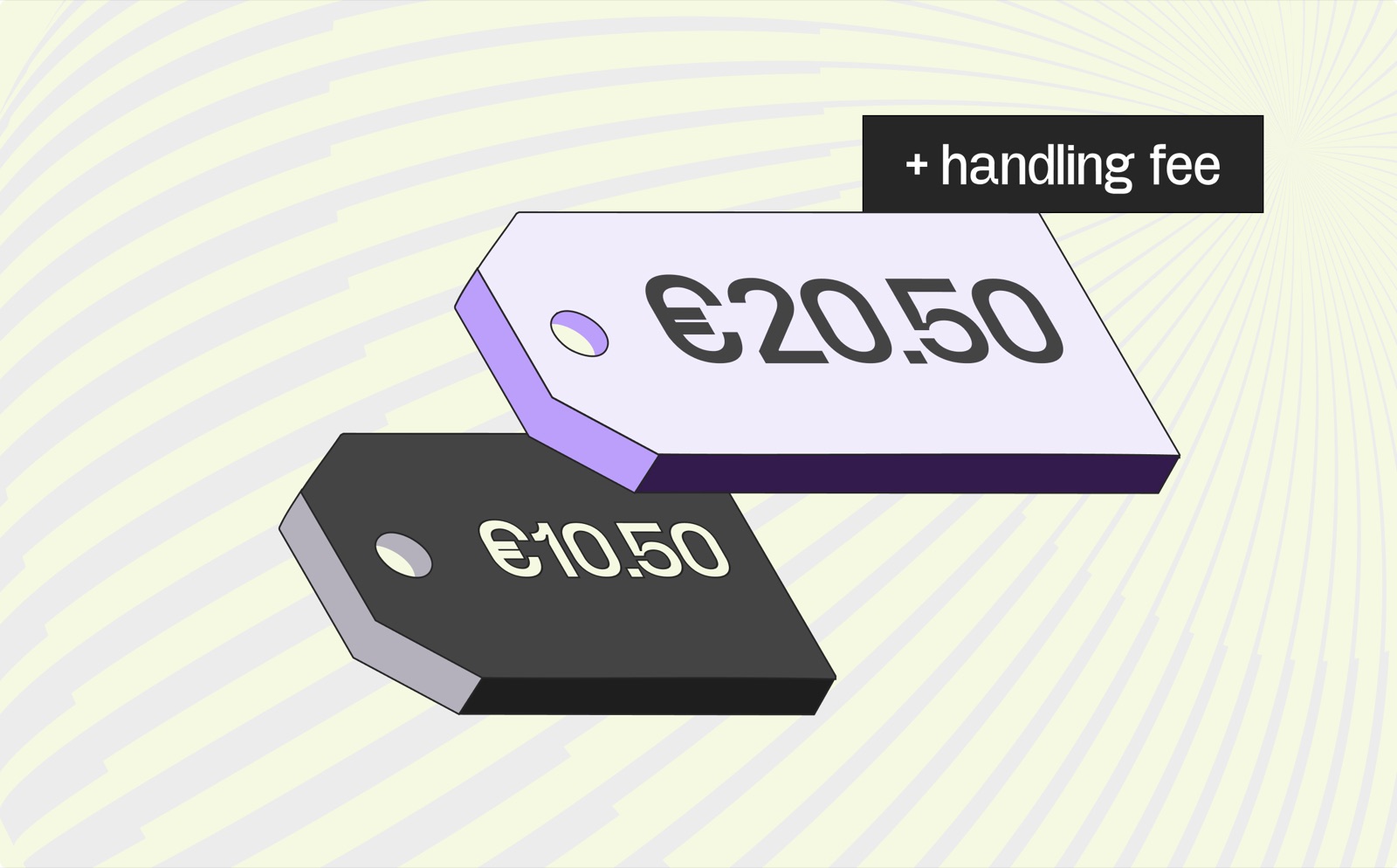

What will it cost? The €50 hoodie

A €50 hoodie shipped from Shein to Amsterdam, across the three eras:

| Per €50 hoodie | Today | Interim (2026–28) | Post-reform (2028+) |

|---|---|---|---|

| Customs value | €50.00 | €50.00 | €50.00 |

| Duty | €0.00 (de minimis) | €3.00 (flat) | €6.00 (~12% tariff) |

| Handling fee | €0.00 | €2.00 | €0.00 (platform absorbs) |

| Import VAT (21%) | €10.50 | €11.55 | €11.76 |

| Total landed price | €60.50 | €66.55 | €67.76 |

(Post-reform figures assume classification-based duty once the Data Hub is live; exact treatment depends on final law.)

The headline isn’t the ~€7 rise. It’s who handles it, and where. Today the cost can ambush the customer at the door — a €10.50 VAT bill arriving as a €20.50 “pay or we return it” text, once you add a courier handling fee. From 2028 it has to be priced in at checkout, by whoever is the importer of record.

How should sellers prepare?

Strip away the phases and the reform does one thing: it forces accurate customs data upstream and moves the legal liability onto whoever sells the goods. “We didn’t know” stops being an option.

That leaves two choices. Become the Importer of Record yourself — stand up entities, register, classify every SKU to the right HS code, calculate CIF, collect duty and VAT at checkout, and own the audit risk. Or hand that liability to infrastructure that already runs it.

That second option is Customs of Record. Outpost becomes the legal importer of record on cross-border parcels, absorbs the duty and import-tax liability, classifies goods with an HS-code engine instead of a spreadsheet, and makes the landed price honest at checkout — so your customer never gets the surprise text and you never get the fine. It’s the physical-goods sibling of Outpost’s Merchant of Record model, which carries the sales-tax and VAT liability on digital sales. The old question was “how much duty do I owe?” From 1 July 2026, the only one that matters is “who carries the risk?”

FAQ

When does EU de minimis end?

The €150 customs-duty exemption is abolished on 1 July 2026. From that date every parcel entering the EU faces duty, starting with an interim €3 flat charge per item-category.

What is the EU €3 flat duty?

A transitional flat customs duty of €3 per item-category (HS tariff line) on low-value parcels under €150, applied from 1 July 2026 until the EU Customs Data Hub replaces it with classification-based duty (targeted 2028).

What’s the difference between import duty and import VAT?

Import duty is a sunk cost — a percentage of customs value you never recover. Import VAT is a consumption tax that VAT-registered businesses can usually reclaim. Duty is set by the HS code (i.e. TARIC in the EU); VAT is set by the destination country.

What is IOSS and why does it matter?

The Import One-Stop Shop lets sellers collect EU import VAT at checkout so parcels clear customs automatically. Without it, the buyer gets a surprise bill plus a courier handling fee at the door.

Who becomes the importer of record in 2028?

Under the deemed-importer rule, large platforms (e.g. Amazon, Temu, Shein) become the legal importer and must collect duty and VAT at checkout — ending the surprise bill by law. Sellers off those platforms need their own importer-of-record solution.

Ready to take customs off your balance sheet?

See how Outpost becomes the importer of record on your cross-border parcels — absorbing the duty and import-tax liability and pricing the landed cost honestly at checkout, so 1 July 2026 lands as a pricing update, not a fire drill.

This article explains EU customs reform for general information and isn’t legal or tax advice. Several figures — the per-item duty basis, the ~€2 handling fee, and the post-2028 tariff bands — are still being finalised; confirm the current rules before acting. For advice specific to your business, consult a qualified customs or tax professional.